As the year draws to a close, it’s important that we discuss any year-end strategies that might help lower your business’s taxable income for 2025.

As the year draws to a close, it’s important that we discuss any year-end strategies that might help lower your business’s taxable income for 2025.

This has been a big year for tax law changes, with the President signing the One Big Beautiful Bill Act (OBBBA) into law this summer. Most of the changes are highly favorable to businesses, and most apply retroactively to the beginning of the year.

The following is a recap of the new and expanded tax breaks and other key changes, along with a few other tax items to consider as the year draws to a close. Let me know if there are any provisions you’d like to discuss:

NEW AND EXPANDED TAX BREAKS

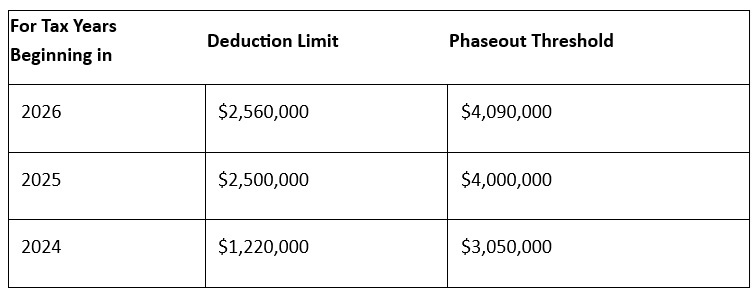

Section 179 Expensing Limit Doubled

Section 179 Expensing Limit Doubled. Section 179 expensing got a big boost from the OBBBA, which more than doubles the dollar limit on the deduction from $1.22 million to $2.5 million. The deduction limit is reduced on a dollar-for-dollar basis (i.e., phased out) by any amount by which the cost of Section 179 property placed in service during the year exceeds a threshold amount as follows:

Passenger automobiles subject to the “luxury car” depreciation limitation are eligible for Section 179 expensing only to the extent of certain dollar limitations ($12,200 for 2025). For sport utility vehicles above the 6,000-pound weight rating and not more than the 14,000-pound weight rating, which are not subject to the luxury car limitation, the maximum cost that may be expensed for 2025 under Section 179 is $31,300.

Planning Opportunity: If your Section 179 expensing was constrained by the $1.22 million limit in 2024, it’s going to be a lot less constrained in 2025, assuming the phaseout doesn’t come into play. Keep in mind that one of the big advantages of Section 179 expensing (as compared to bonus depreciation) is that it allows you to pick and choose which individual assets you expense, and even what portion of the cost of each asset you expense, making it a very precise and flexible tax planning tool.

100 Percent Bonus Depreciation Made Permanent

100 Percent Bonus Depreciation Made Permanent

Under rules enacted by the Tax Cuts and Jobs Act (TCJA), bonus depreciation was scheduled to be repealed for property placed in service after 2026 (2027 for longer production period property and aircraft), culminating a multi-year phaseout of the deduction. Under these rules, the bonus depreciation percentage was 40 percent for property placed in service in 2025 (60 percent for longer production period property and aircraft).

The OBBBA permanently increases the bonus depreciation percentage to 100 percent for all qualified property acquired after January 19, 2025, as well as for specified plants planted or grafted after that date. The new law made only one change to the definition of qualified property: it added qualified sound recording productions to the list of eligible property.

Planning Opportunity: The OBBBA provides a transitional rule that will allow your business to elect to apply a 40 percent bonus depreciation percentage (60 percent for longer production period property and aircraft) in the first tax year ending after January 19, 2025. Although it’s usually advantageous to apply the maximum bonus depreciation percentage allowed, there are situations where choosing a lower percentage can make sense (for example, to avoid creating a net operating loss).

Full Expensing of Domestic Software Development and R&E Expenditures

Full Expensing of Domestic Software Development and R&E Expenditures

Reversing TCJA rules that had been in effect since 2022, the OBBBA restores full expensing for domestic software development and research or experimental expenditures (“R&E expenditures”). It leaves in place the rules requiring that foreign software development and R&E expenditures be capitalized and amortized over 15 years.

The OBBBA also provides a rule that allows “small” businesses with annual gross receipts of $31 million or less to apply the new expensing rules retroactively to tax years beginning after December 31, 2021 by filing amended returns (or, under certain conditions, an original return). In addition, any business (small or large) can write off unamortized domestic software development and R&E expenditures that were capitalized under TCJA ratably over a one- or a two-year period, beginning with the business’s first tax year beginning after December 31, 2024. Businesses will continue to have the option of capitalizing domestic software development and R&E expenditures and amortizing them over a period of at least 60 months.

Planning Opportunity: If your business capitalized domestic software development or R&E expenditures for tax years after December 31, 2021, the options for writing them off on an accelerated basis (or filing amended returns) create some fantastic tax planning opportunities. We should discuss them at your earliest convenience.

Special Depreciation Allowance for Qualified Production Property

Special Depreciation Allowance for Qualified Production Property

The OBBBA designates a new category of property referred to as “qualified production property” and allows businesses an additional first-year depreciation deduction equal to 100 percent of the adjusted basis of such property.

Qualified production property is essentially nonresidential real property in the United States (or any possession) used for manufacturing and placed in service after July 4, 2025 and before January 1, 2031. In this context, “manufacturing” means producing or refining a product in a way that results in a substantial transformation of the property comprising the product.

Qualified production property does not include the portion of any nonresidential real property used for offices; administrative services; lodging; parking; sales activities; software development or engineering activities; or other functions unrelated to manufacturing, production, or refining of tangible personal property.

Recapture Rules: If the use of the qualified production property changes during the 10-year period after the property is placed in service, recapture rules generally apply.

Return to EBITDA for Limit on Business Interest Deduction

Return to EBITDA for Limit on Business Interest Deduction

For tax years beginning after December 31, 2024, the OBBBA increases the cap on the deductibility of business interest expense by providing that “adjusted taxable income” is determined without taking into account deductions for depreciation, amortization, or depletion. As a result, “adjusted taxable income” corresponds with the financial accounting concept of earnings before interest, taxes, depreciation, and amortization (EBITDA). This restores a rule that was in effect from 2018-2022.

The OBBBA also changes the rules for coordinating the cap on business interest expenses with the rules for interest capitalization. The new rules require that the business interest limitation be calculated prior to the application of any interest capitalization provision, and that capitalized interest be given priority in utilizing the cap.

Qualified Business Income Deduction

Qualified Business Income Deduction

The OBBBA permanently extends the Section 199A deduction for qualified business income that had been set to expire on December 31, 2025. For tax years beginning after 2025, the size of the fixed range of taxable income over which the wage and investment limitation and the SSTB limitation are phased in is increased from $100,000 to $150,000 for married individuals filing joint returns, and from $50,000 to $75,000 for all others.

For tax years beginning after 2025, the OBBBA also introduces a new, inflation-adjusted, minimum deduction of $400 for taxpayers who have at least $1,000 of QBI from one or more active trades or businesses in which the taxpayer materially participates.

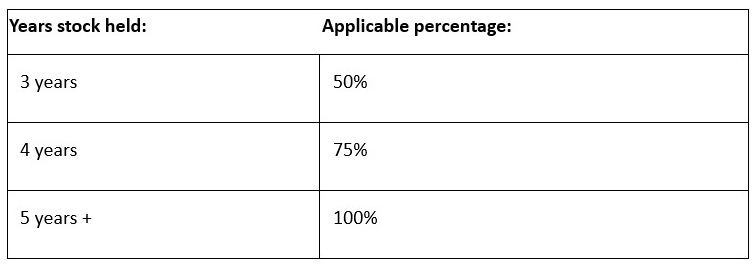

Expansion of Qualified Small Business Stock Gain Exclusion

Expansion of Qualified Small Business Stock Gain Exclusion

Since it was introduced in 1993, owners of Section 1202 qualified small business stock (QSBS) have been required to hold their stock for at least five years before they could exclude gain from its sale from income. Those exclusions ranged from 50 to 100 percent, depending on when the stock was acquired.

The OBBBA enhances the QSBS gain exclusion by providing a tiered gain exclusion for stock acquired after July 4, 2025, as follows:

For stock acquired after July 4, 2025, the OBBBA also increases the per-issuer exclusion cap to $15 million, and the corporate-level aggregate-asset ceiling to $75 million. Both the $15 million exclusion cap and the $75 million asset ceiling are indexed for inflation beginning in 2027.