Taking the Standard Deduction Versus Itemizing

Taking the Standard Deduction Versus Itemizing

The Tax Cuts and Jobs Act (TCJA) substantially increased the standard deduction amounts, thus making itemized deductions less attractive for many individuals. The OBBBA makes this change permanent. For 2025, the standard deduction amounts are: $15,750 (single); $23,625 (head of household); and $31,500 (married filing jointly).

If the total of your itemized deductions in 2025 will be close to your standard deduction amount, we should evaluate whether alternating between bunching itemized deductions into 2025 and taking the standard deduction in 2026 (or vice versa) could provide a net-tax benefit over the two-year period. For example, you might consider doubling up this year on your charitable contributions rather than spreading the contributions over a two-year period. Adjusting the timing of your payments of state income taxes, property taxes, and medical bills can also help.

Bear in mind that even if you haven’t itemized in recent years, the big increase in the limit on the SALT deduction mentioned above may change the math in favor of itemizing. If you’re not sure where you stand, let’s run the numbers and find out. In years when it applies, itemizing can shave thousands of dollars (sometimes much more) off your tax bill. So it’s worth spending a little time to find out if we should change our approach in response to the favorable changes in the rules.

SALT Refresher

SALT Refresher

Because of the $10,000 cap on this deduction in recent years (2018-2024), it may have been a while since you’ve had to think about how to max out your deduction. Here’s a quick refresher on what you can deduct:

* state and local income taxes;

* property taxes on real estate;

* personal property taxes (typically on motor vehicles); and

* sales tax, but only as an alternative to deducting state and local income taxes.

If you choose to deduct your sales taxes, you can either keep records of the actual sales taxes you pay during the year, or let us determine the deductible amount using tables provided by the IRS.

Motor vehicle taxes or fees must be based on the value of your vehicle to be deductible. Taxes and fees based on weight, model year, and/or horsepower are not deductible. But taxes or fees that are partly based on value and partly based on other criteria may qualify in part.

As mentioned before, the SALT deduction limit is $40,000 for 2025, and it starts phasing down to the old $10,000 limit when your AGI reaches $500,000. If you’re married and file separately, the limit is $20,000, and the phase down starts at AGI of $250,000.

Medical Expenses

Medical Expenses

For 2025, your medical expenses are deductible as an itemized deduction to the extent they exceed 7.5 percent of your AGI. To be deductible, medical care expenses must be primarily to alleviate or prevent a physical or mental disability or illness. They don’t include expenses that are merely beneficial to general health, such as vitamins or a vacation.

Deductible expenses include the premiums you pay for insurance that covers the expenses of medical care, and the amounts you pay for transportation to get medical care. Medical expenses also include amounts paid for qualified long-term care services, and limited amounts paid for any qualified long-term care insurance contract.

Depending on what your taxable income is expected to be in 2025 and 2026, and whether itemizing deductions would be advantageous for you in either year, you may want to accelerate any optional medical expenses into 2025 or defer them until 2026. The right approach depends on your income for each year, expected medical expenses, as well as your other itemized deductions.

Charitable Contributions

Charitable Contributions

If you are itemizing deductions, you can maximize the tax benefit of making a charitable contribution by donating appreciated assets, such as stock, instead of cash. Doing so generally allows you to deduct the fair market value of the asset while also avoiding the capital gains tax that would otherwise be due if you sold the asset. The more highly appreciated the asset, the better this strategy works.

Charitable contributions are highly useful for year-end tax planning because you have great control over both the amount and the timing. That’s not to say that you should let the tail wag the dog: if you enjoy making contributions during the holiday season or some other time of year that’s meaningful to you, changing the timing of your contributions for tax reasons may not be worth it. But it can’t hurt to be aware that there can be a big difference from a tax standpoint between making a contribution in late December versus early January.

2026 Change Alert: If you make substantial contributions in some years and not others, there’s a good reason why you might want to choose 2025 over 2026. Beginning in 2026, if you itemize, your charitable contribution deduction will be reduced by 0.5% of your AGI. For example, if your income is $200,000, your deduction will be reduced by $1,000. No such rule applies in 2025.

Charitable Contributions Directly from Your IRA: If you have an individual retirement account and are 70 1/2 years old and older, you are eligible to make charitable contributions directly from your IRA. You don’t get a deduction for such contributions, but you don’t have to include the amount in your income. This can be advantageous compared with taking a distribution and making a donation to the charity that may or may not be deductible as an itemized deduction. It can also be advantageous from a standpoint of lowering your AGI, which can help reduce taxes on your Social Security income, reduce any net investment income tax, and preserve your ability to claim various deductions that are phased out or reduced based on your income.

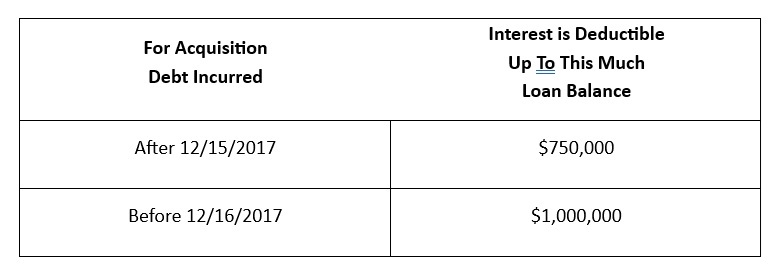

Mortgage Interest Deduction

Mortgage Interest Deduction

If the mortgage on your principal residence has a balance of $750,000 or less, your mortgage interest will generally be fully deductible. If your loan balance is higher than $750,000, deductibility depends on when you incurred the debt:

The same limit that applies to your original mortgage applies to any refinancings. If your loan balance increases when you refinance (i.e., a “cash out” refinancing), the interest on the additional loan balance is only deductible to the extent you used the funds to substantially improve your home. If you operate a business from your home, any loan balance/interest we allocate to the business is not subject to the above limits.

Interest on Home Equity Loans

Interest on Home Equity Loans

You can potentially deduct interest paid on home equity indebtedness, but only if you used the debt to substantially improve your home.

Thus, for example, interest on a home equity loan used to build an addition to your existing home is typically deductible, while interest on the same loan used to pay personal expenses, such as credit card debt, is not. The balance of any home equity loans is added to the balance of your mortgage for purposes of applying the $750,000/$1,000,000 limits discussed above.

Mortgage Insurance Premiums

Mortgage Insurance Premiums

Beginning in 2026, you can deduct mortgage insurance premiums as mortgage interest. The deduction is phased out for AGI above $100,000 ($50,000 for married filing separately).

Student Loan Interest

Student Loan Interest

You can deduct up to $2,500 of interest paid on a qualified education loan in computing AGI. This is an above-the-line deduction, so you do not have to itemize to claim it. In 2025, the deduction is phased out for AGI above $170,000 for married filing jointly, and $85,000 for all others.

Sale of a Home

Sale of a Home

If you sold your home this year, and it was your principal residence for at least two of the five years before the sale, you can exclude from income up to $250,000 of your gain on the sale ($500,000 if you’re married filing jointly and meet a few conditions). Your taxable gain is also reduced by any amounts that you spent on improvements and additions that add to the value of a residence, prolong its useful life, or adapt it to new uses. If you think your gain might exceed the $250,000/$500,000 exclusion, you’ll want to put together records of any improvements you made to the home, which we can use to reduce your gain. We’d be happy to send you examples of what qualifies as an improvement for tax purposes and what doesn’t.

Note that if you rented out your home or used part of it for business purposes, your exclusion may be reduced. The reduction generally does not apply if you rent your home out for less than three years between the date you moved out and the date you sold it, as long as it was your principal residence prior to that. A loss on the sale of a principal residence is generally not deductible. But if you rented out your home or used it for business, the loss attributable to that portion of the home is deductible.