The One Big Beautiful Bill Act is mostly very good news for businesses. But the sweeping bill also includes several provisions that will increase the tax bills of some businesses, including the repeal of some popular tax breaks.

Excess Business Losses of Noncorporate Taxpayers

Excess Business Losses of Noncorporate Taxpayers

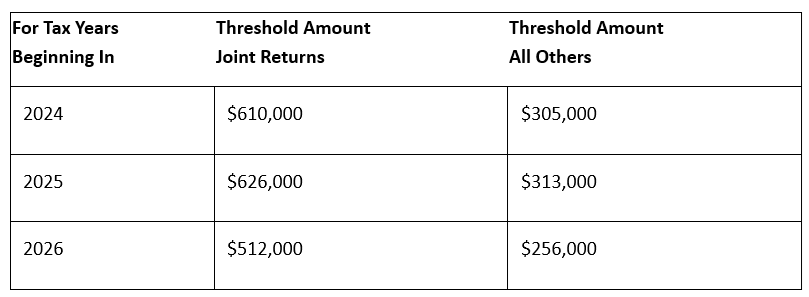

The OBBBA makes permanent the rules that disallow the deduction of “excess business losses” by noncorporate taxpayers. Excess business losses are the excess of current-year net business losses over an inflation-indexed threshold amount (see table below). The OBBBA also resets the base year for inflation indexing of the threshold from 2018 to 2025, resulting in a decrease in the threshold in 2026:

One Percent Floor on Charitable Contributions by Corporations

One Percent Floor on Charitable Contributions by Corporations

The OBBBA keeps in place the longstanding 10-percent limit on the deduction for corporate charitable contributions, and adds a 1 percent floor. For tax years beginning after December 31, 2025, a corporate taxpayer may claim a deduction for charitable contributions only to the extent that total contributions exceed one percent of its taxable income, and does not exceed 10 percent of its taxable income.

Excise Tax on Remittance Transfers

Excise Tax on Remittance Transfers

For transfers made after 2025, the OBBBA imposes a 3.5 percent excise tax on remittance transfers. The tax is paid by the sender and collected by remittance transfer providers. For purposes of the new tax, remittance transfers are cross-border transfers of cash or similar instruments between U.S. senders and recipients in foreign countries.

Repeal of Clean Energy Tax Breaks for Businesses

Repeal of Clean Energy Tax Breaks for Businesses

The OBBBA terminates several clean energy tax breaks for businesses enacted by the Inflation Reduction Act of 2022 by moving up their expiration dates. (Most were scheduled to expire at the end of 2032 or 2034.)

– The qualified commercial clean vehicle credit is terminated for vehicles acquired after September 30, 2025.

– The energy efficient commercial buildings deduction is terminated for construction beginning after June 30, 2026.

– The alternative fuel vehicle refueling property credit is terminated for property placed in service after June 30, 2026.

– The clean hydrogen production credit is terminated for facilities the construction of which begins on or after January 1, 2028.

– The special five-year cost recovery period for certain energy property is terminated for construction beginning after December 31, 2024.

The OBBBA also curtailed the availability of several other clean energy credits, most notably the clean electricity production credit.

Rental Real Estate

Rental Real Estate

If you have any rental real estate activities, it’s important to determine if the activity will be considered a passive activity by the IRS.

Generally, losses from passive activities are only deductible against passive activity income. However, a deduction of up to $25,000 ($12,500 if married filing separately) may be allowed against nonpassive income to the extent you actively participate in the rental real estate activities.

This deduction is subject to a phaseout for individuals with modified adjusted gross income above $100,000 (or $50,000 if married filing separately). Additionally, you may be eligible for a qualified business income deduction if certain criteria are met, such as the rental activity qualifying as a Section 162 trade or business.

Substantiation of Vehicle-Related Deductions

Substantiation of Vehicle-Related Deductions

In audits, the IRS tends to focus on deductions taken for vehicle expenses. If not properly substantiated, such deductions are disallowed. Thus, if vehicles are used in any part of your business or business-related activities, your tax records with respect to each vehicle should include the following:

* the amount of each separate expense with respect to the vehicle (e.g., the cost of purchase or lease, the cost of repairs and maintenance, etc.);

* the amount of mileage for each business or investment use and the total miles for the tax period;

* the date of the expenditure; and

* the business purpose for the expenditure.

The IRS will consider the following as adequate substantiation for such expenses: (1) records such as a notebook, diary, log, statement of expense, or trip sheets; and (2) documentary evidence such as receipts, canceled checks, bills, or similar evidence.

It’s important to note that records are considered adequate to substantiate the element of a vehicle expense only if they are prepared or maintained in such a manner that each recording of an element of the expense is made at or near the time the expense is incurred.

Employee Benefits

Employee Benefits

One area I would like to discuss with you is the tax and other advantages your business could reap by offering a retirement plan and/or other fringe benefits to employees. By offering such benefits, your business has a better chance of attracting and retaining talented workers which, in turn, reduces the costs of searching for and training new employees. Contributions made to retirement plans on behalf of employees are deductible, and your business may be eligible for tax credits for offering retirement and other benefits.

If you haven’t already done so, you might consider the establishment of a flexible spending arrangement (FSA). An FSA allows employees to be reimbursed for medical expenses and is usually funded through voluntary salary reduction agreements with the employer. The employer has the option of making or not making contributions to the FSA. Some of the benefits of providing an FSA for employees include contributions made by the business being excluded from the employee’s gross income; reimbursements to the employee are tax-free if used for qualified medical expenses; the FSA can be used to pay qualified medical expenses even if the employer or employee haven’t yet placed the funds in the account; and up to $660 of funds in the FSA can be carried over to subsequent years indefinitely.

Another popular employee benefit your business might consider is a high deductible health plan paired with a health savings account (HSA). The benefits to your business include savings on health insurance premiums that would otherwise be paid to traditional health insurance companies, and having employee wage contributions to the plan not being counted as wages, and thus neither the employer nor the employee is subject to FICA taxes on the payroll contributions. As for employees, they can reap a tax deduction for funds contributed to the HSA, and there is no use-it-or-lose-it limit like there is for most flexible spending arrangements (FSAs). Thus, the funds can grow tax-free and be used in retirement.

Businesses that do not already sponsor a retirement plan can offer a “starter” 401(k) plan. A starter 401(k) plan generally requires that all employees be default enrolled in the plan at a 3 to 15 percent of compensation deferral rate. Employer contributions are not permitted. The limit on annual deferrals is the same as the IRA contribution limit (for 2025, $7,000 with an additional $1,000 in catch-up contributions for employees age 50 or older).

Pass-Thru Entity Considerations

Pass-Thru Entity Considerations

If you are operating a business through a pass-thru entity such as a partnership or S corporation, your basis in the entity must be high enough to allow for any loss deduction, if you have one for the year. In such a situation, we should consider the options available for increasing your basis in such entity.

If you are an S corporation shareholder, it’s important to ensure that you and other shareholders involved in running the business are paid an amount that is commensurate with the work being done. The IRS scrutinizes S corporations which distribute profits instead of paying compensation subject to employment taxes. Failing to pay arm’s length salaries can lead to tax deficiencies, interest, and penalties. The key to establishing reasonable compensation is showing that the compensation paid for the type of work an owner-employee does for the S corporation is similar to what other entities would pay for similar work. An S corporation needs to adequately document the factors that support the salary an S corporation owner is being paid.

Also, because there are stringent requirements for who may be an S corporation shareholder, if the number of shareholders has changed or increased during the year, we should review the residency or citizenship status of the S corporation’s shareholders and S corporation stock beneficiaries (including contingent and residuary beneficiaries).

Concluding Thoughts

Concluding Thoughts

As you can see, there is much to consider before we prepare your 2025 business tax return and calculate any estimated tax payments that might be due in 2026. Please call me at your convenience so we can set a time to meet and review potential strategies for reducing your business’s 2025 taxable income and tax liability.